Regular readers know we're concerned about the long-term health of the U.S. dollar. It's the central theme of Porter's "End of America" thesis. (His video has been viewed more than 20 million times.) In short, the U.S. government is headed for a slow-motion default on its debts and obligations.

While we can't predict where the value of the dollar will be five years from now, we can comfortably predict it will get to that value with great volatility. Most Americans will be rocked by this volatility. S&A readers will be prepared for it... and should be positioned to prosper from it.

The answer is A LOT.

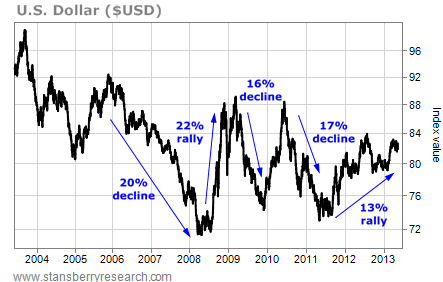

Below is a 10-year chart of the U.S. dollar index. It measures the dollar's value against a basket of foreign currencies, like the Japanese yen and the euro. It's the generally agreed-upon measure of the dollar's global trade value.

One glance at the chart below, and you'll see that our prediction of currency volatility isn't outlandish. It displays the value of our bank accounts. And it's bouncing up and down with tremendous volatility. Double-digit percentage changes in value are taking place in the span of months... not years.

Think holding U.S. dollars in a bank account is a boring, conservative idea? Think again.

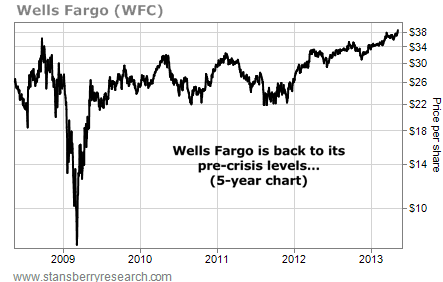

Wells Fargo just announced it would expand its small-business lending. The company is placing more than 1,500 additional loan experts in local branches and expanding its portfolio of credit products. The stock hit a new high this week, reaching its pre-crisis peak.

According to The Wall Street Journal, the moves come after loans to commercial and industrial companies expanded at an 11% annualized rate in the first quarter. That's the sixth double-digit gain in the last seven quarters. More than one-quarter of U.S. banks have cut their credit costs.

Retirement Millionaire subscribers who bought Wells Fargo on Doc's recommendation are up 16% since April 2012.

Half the offering was $500 million of five-year debt yielding 1.3%, just 0.57% over comparable Treasurys. The rest was in 30-year debt yielding 4.3%, 1.35% over comparable Treasurys.

During Saturday's Berkshire Hathaway annual meeting in Omaha, Nebraska, which I (Dan Ferris) attended, Buffett said he felt sorry for people holding on to fixed-dollar investments. He said holding cash and Treasurys has been "brutal."

Richard Cook of Cook & Bynum Capital Management in Birmingham, Alabama, told Bloomberg that "Berkshire issuing debt is effectively an efficient way [for Buffett] to short the bond market." If you don't understand the comment, think about it. Buffett isn't buying bonds, he's selling them. Shorting means selling.

We're intrigued by one of the recommendations that was reported on...

"I hate the chart, I like the products," he said. "I do not like the price-to-earnings (P/E) ratio. I am not impressed with earnings growth... I am not attracted to anything related to middle-class consumer discretionary income... All you need to compete with CMG's core business is a taco truck."

Those comments are silly. Chipotle trades at close to 40 times earnings. That's too expensive for me to buy, but it grows like a weed on steroids. Sales have doubled the last five years and earnings have risen 270%. Chipotle is consistently profitable, with double-digit net margins. The number of restaurants is up 30% in the last three years. If the P/E ratio were 90, that'd be really crazy. But at 40, it's just a little stretched.

And saying a taco truck can compete with it is just plain ridiculous. It's like saying all you need to compete with McDonald's is burger patties and a flattop grill.

Regards,

S&A Research

No comments:

Post a Comment