Richard Levine/Alamy These aren't the best of times for discount retailers, but it certainly seems as if Family Dollar (FDO) has become the belle of the marked-down ball. Two chains catering to thrifty-minded shoppers have entered into an unlikely bidding war for Family Dollar, and it's shaping up to be a bit more interesting than your typical love triangle between three retailers with the name "Dollar" in their monikers. The story began late last month when Family Dollar announced that it would be acquired by Dollar Tree (DLTR) in an $8.5 billion transaction. It seemed like a simple enough transaction. Dollar Tree would be paying a reasonable 22 percent premium for Family Dollar. The deal would create a discounting behemoth with 13,000 stores across North America. The combined companies would eventually result in trimming $300 million in annual overhead. It seemed like a great way out for frustrated Family Dollar shareholders. The deep discounter had missed Wall Street's profit targets for three consecutive quarters. Analysts see declining profitability on flat sales for its fiscal year that ends this week. It seemed as if Dollar Tree would have Family Dollar all to itself, but then it got some unexpected company. Turning Down a Fistful of Dollars Dollar General (DG) stepped into the picture last week, offering to pay even more for Family Dollar. It offered an all-cash deal valued closer to $9 billion. The deal seemed to be clearly superior on the surface, but Family Dollar's board shot it down. This wouldn't be the first time that a board sided with a friendly buyout offer to a higher hostile one. Arranged deals often mean cushier positions for the acquired company. However, there was a method to the board's madness this time. Family Dollar declined Dollar General's offer because it felt that antitrust regulators wouldn't let that particular buyout go through. Dollar General rings up more than twice as much in sales as Dollar Tree. The bigger the rivals are, the larger hurdle that they have to clear for a corporate combination to go through. However, despite the "Dollar" name in the signage of all three, the chains aren't all alike. Dollar Tree is a true dollar store. It's North America's leading operator of discount variety stores where everything sells for a buck or less. Family Dollar and General Dollar are traditional deep discounters, offering general merchandise at various price points. They do help shoppers stretch their dollars, but they're not dollar stores like Dollar Tree. The Buck Stops Here Offering shoppers bargains isn't enough anymore. Walmart (WMT) -- the world's largest retailer and a bellwether when it comes to discount department stores -- has posted flat or negative comparable-store sales at its U.S. stores for six consecutive quarters. "Cheap chic" discount department store operator Target (TGT) has also been posting uninspiring sales, clocking in with flat store-level sales in its latest quarter. Given the dicey environment, it's not a surprise to see deep discounters giving sector consolidation a hand. Family Dollar will get bought out. It may seem as if Dollar Tree has the upper hand with the lower bid, but it remains to be seen if it will have to sweeten its offer. We also can't rule out Dollar General, especially if it agrees to close enough stores to make the deal more likely to clear regulator objections. Investors are encouraged to keep following the "Dollar" signs.

Richard Levine/Alamy These aren't the best of times for discount retailers, but it certainly seems as if Family Dollar (FDO) has become the belle of the marked-down ball. Two chains catering to thrifty-minded shoppers have entered into an unlikely bidding war for Family Dollar, and it's shaping up to be a bit more interesting than your typical love triangle between three retailers with the name "Dollar" in their monikers. The story began late last month when Family Dollar announced that it would be acquired by Dollar Tree (DLTR) in an $8.5 billion transaction. It seemed like a simple enough transaction. Dollar Tree would be paying a reasonable 22 percent premium for Family Dollar. The deal would create a discounting behemoth with 13,000 stores across North America. The combined companies would eventually result in trimming $300 million in annual overhead. It seemed like a great way out for frustrated Family Dollar shareholders. The deep discounter had missed Wall Street's profit targets for three consecutive quarters. Analysts see declining profitability on flat sales for its fiscal year that ends this week. It seemed as if Dollar Tree would have Family Dollar all to itself, but then it got some unexpected company. Turning Down a Fistful of Dollars Dollar General (DG) stepped into the picture last week, offering to pay even more for Family Dollar. It offered an all-cash deal valued closer to $9 billion. The deal seemed to be clearly superior on the surface, but Family Dollar's board shot it down. This wouldn't be the first time that a board sided with a friendly buyout offer to a higher hostile one. Arranged deals often mean cushier positions for the acquired company. However, there was a method to the board's madness this time. Family Dollar declined Dollar General's offer because it felt that antitrust regulators wouldn't let that particular buyout go through. Dollar General rings up more than twice as much in sales as Dollar Tree. The bigger the rivals are, the larger hurdle that they have to clear for a corporate combination to go through. However, despite the "Dollar" name in the signage of all three, the chains aren't all alike. Dollar Tree is a true dollar store. It's North America's leading operator of discount variety stores where everything sells for a buck or less. Family Dollar and General Dollar are traditional deep discounters, offering general merchandise at various price points. They do help shoppers stretch their dollars, but they're not dollar stores like Dollar Tree. The Buck Stops Here Offering shoppers bargains isn't enough anymore. Walmart (WMT) -- the world's largest retailer and a bellwether when it comes to discount department stores -- has posted flat or negative comparable-store sales at its U.S. stores for six consecutive quarters. "Cheap chic" discount department store operator Target (TGT) has also been posting uninspiring sales, clocking in with flat store-level sales in its latest quarter. Given the dicey environment, it's not a surprise to see deep discounters giving sector consolidation a hand. Family Dollar will get bought out. It may seem as if Dollar Tree has the upper hand with the lower bid, but it remains to be seen if it will have to sweeten its offer. We also can't rule out Dollar General, especially if it agrees to close enough stores to make the deal more likely to clear regulator objections. Investors are encouraged to keep following the "Dollar" signs.

Tuesday, August 26, 2014

Why Is There a Bidding War to Buy Family Dollar?

Sunday, August 24, 2014

Apple Might Want To Take Notice Of This Massive Opportunity

Apple's (NASDAQ: AAPL ) expected iPhone 6 launch will most certainly be the biggest device launch of 2014, as the company releases the fourth major refresh to its iPhone family. While the iPhone's hardware, software, and size are all likely to change, consumers and investors still want more from the company.

Since Steve Jobs's passing, many have questioned Apple's ability to innovate and create great products in new markets. Unfortunately, the company has been slow to respond in key industries like wearables, and in one particular space where it is missing a golden opportunity.

The power of Apple

In Apple's last quarter it sold 35.2 million and 13.3 million iPhones and iPads, respectively. Importantly, these enormous numbers came ahead of expected product launches, a period where many thought consumers would wait a few months longer for the newest devices. However, Apple's success demonstrates the power of its brand, where it can release updated versions of existing products and create many billions in annual profit.

Still, in technology, what's in favor with consumers can change quickly. And although Apple has a strong ecosystem filled with consumers and businesses that are interconnected on various devices, we must still wonder when Apple will unleash its next big product.

Planning ahead with new products and services

For all the good things we can say about Apple's hardware, Google (NASDAQ: GOOG ) (NASDAQ: GOOGL ) is just as dominant on the Web and Microsoft (NASDAQ: MSFT ) in software. Yet, neither Google nor Microsoft have grown comfortable in their successful time-tested niche markets, both looking ahead to the next 10 years with new products.

Specifically, Google has taken the broadband Internet market by storm with Fiber, a multi-billion dollar project that increases Internet speeds by up to 100 fold versus the average broadband provider. For Microsoft, it has embraced the cloud, specifically cloud infrastructure and application platforms to become a viable competitor against the juggernaut Amazon.com. As a result, Microsoft and Google have their own insurance policy beyond their flagship industries to create growth in the decade ahead.

Apple should take notice

For Apple, it's already late to the wearables market, and even with the Beats acquisition, music isn't really a game-changer for a company with $180 billion in revenue. However, there is one market where it could thrive with its premium pricing and services strategy, a market that is growing especially fast, smart TVs.

Apple has been long-rumored as a company that could enter the TV space, but nothing official yet. Of course, the company has Apple TV, which connects users to movies and shows via iTunes along with photos, music, and Internet content. In total, Apple has sold 20 million of these devices, including seven million over the last year, creating more than $1 billion in revenue from media content in the 12-months prior to April of this year.

Therefore, Apple has the foundation for an entrance into the smart TV space, but desperately needs the corresponding hardware, with now being the time to strike.

According to BI Intelligence, 75 million smart TVs shipped globally in 2013, and 101 million are expected this year. Then, in 2015 smart TVs shipments are expected to surpass traditional TV shipments with 124 million, followed by 148 million and 172 million in the following two years, respectively. Therefore, from 2013-2017, smart TVs are a business that's growing at an annualized rate of 23% -- which is actually faster than the rate of e-commerce growth in the U.S -- and will eventually own nearly 75% of the total TV market.

As a result, with the smartphone and tablet markets both reaching maturity in the U.S. it seems logical that Apple would take such data in stride, and make an aggressive push into the smart TV space as its next big-time market.

Falling prices should not be a concern

Now, one reason that investors reject the idea of Apple creating a smart TV is because the price of TVs in general have collapsed in the last decade. Back in 2005, the average 32-inch LCD TV cost $1,566 , then $729 in 2007, and in 2012 fell to just $435. Today, most 32 inch TVs can be purchased for under $350, and while smart TVs command a slight premium, its prices have also seen rather aggressive declines in the last several years.

With that said, consumers and investors tend to forget that when cell phones were first introduced, they were expensive luxuries that only the wealthy could afford, and gradually saw price declines over time. In fact, Whiteboard Advisors estimates that the average price of a cell phone in 1984 was $4,000 after being adjusted for inflation. Still, Apple has managed to become the most valuable company in the world despite these lower prices, and has been able to demand higher prices due to the luxury of its product.

Foolish Thoughts

In other words, price decline worries are irrelevant as it applies to Apple not entering the smart TV space, and investors should realize that Apple is missing a golden opportunity by not acting on an industry that's expected to ship 124 million units next year. With all of Apple's devices being connected, there's no doubt that a smart TV would be a big hit with consumers, and could be meaningful for the company's fundamental performance.

Leaked: Apple's next smart device (warning, it may shock you)

Apple recently recruited a secret-development "dream team" to guarantee its newest smart device was kept hidden from the public for as long as possible. But the secret is out, and some early viewers are claiming its everyday impact could trump the iPod, iPhone, and the iPad. In fact, ABI Research predicts 485 million of this type of device will be sold per year. But one small company makes Apple's gadget possible. And its stock price has nearly unlimited room to run for early in-the-know investors. To be one of them, and see Apple's newest smart gizmo, just click here!

Friday, August 15, 2014

Lightstream (LTS) – When The Market Freaks Out, Rejoice

Lightstream (which I've covered in-depth here and here) reported results last week (here). Included in those results was a downward revision to 2014 production volume, from 44k boe / d to 42k boe / d. The market did not take too kindly to the Company's lower forecast, sending the stock down 10%.

But the market isn't paying attention to the right things. And investors that know better should rejoice because acquiring ownership in LTS just became a lot cheaper. It's a mantra that needs to be hung on every investor's wall:

When the market freaks out and you know better, rejoice.

To the informed investors of Lightstream, this is what matters:

Sustainability should get to 100% or better this year. Base decline continues to meet plans and will come in at 26% – 29% for the full year. Debt is down to $1.89BN. On Swan Hills – the problem area that sent forecasted production volume lower – the wells are still good oil wells. 7 wells are collectively producing 1,450 boe / d instead of 2,000 boe / d. Management noticed the deviation from expectations and immediately pushed pause to figure out why. This is what every prudent business owner should do.What's interesting – and a point the market has clearly ignored – is that funds flow (operating cash flow after interest expense) is still expected to meet guidance. I repeat: there was no change to projected cash flow.

Looking at the Company's new guidance, FCF is expected to be $85MM – $165MM. To get to sustainability, take out the approx. $95MM in 2014 dividends. The midpoint implies $30MM in cash buildup – that's after CapEx, interest and all dividends. This means that the market's biggest concern about Lightstream – the sustainability of their business model – is no longer a concern. The inflection point of sustainability has arrived. And that is what matters.

| Currently 0.00/512345 Rating: 0.0/5 (0 votes) |

Tuesday, August 12, 2014

Stocks: All This and Nothing

A whole lot of nothing and a little bit of everything helped stocks finish in the red today.

AP

AP The S&P 500 fell 0.2% to 1,933.75, while the Dow Jones Industrial Average dipped 0.1% to 16,560.54. The Nasdaq Composite dropped 0.3% to 4,389.25 and the small-company Russell 2000 got walloped to the tune of 0.8% to 1,133.03.

There was little in the way of major news today. Germans aren’t feeling very confident. Russia is sending ‘aid’ to Ukraine, a decision some worry could be a pretext for an invasion. Israelis and Palestinians still can’t get along. The U.S. said that its attacks have failed to stop the ISIS advance.

JPMorgan’s David Kelly ponders the “sour mood of the public” towards the stock market:

According to polling by Rasmussen Reports in early August, currently 49% of Americans believe the economy is in recession, 32% believe it is not and 19% aren't sure. This is a startling result given that we are now in the sixth year of economic expansion with an unemployment rate just 0.1% above its 50-year average of 6.1%…

This surprisingly glum mood (given broadly improving economic statistics) could reflect a general mistrust of Washington – both Congress and the President are scoring low in approval ratings and many fear the eventual result of very easy money from the Federal Reserve. Or it could reflect the widening income and wealth gap which has prevented the majority of Americans from experiencing much of the economic recovery.

However, whatever the reason for the still negative public mood, it is important not to allow it to guide investment decisions except to the extent that this mood impacts investment fundamentals…

A generally negative feeling about the state of America is no reason to avoid equities. If the last 15 years have taught us anything about investing, surely it is that the winners tend to be those who invest based on how they think, rather than how they feel.

Morgan Stanley’s Adam Parker and team discuss what would cause them to get bearish:

Our view is that hubris and debt define the top of every cycle, and as such, we monitor signs of growing costs that could ultimately translate into more downside to corporate earnings. Today, it is very hard to make that argument. In fact, we think it is possible that capital intensity is now peaking for the biggest 1500 US companies, at just less than 7% of sales (Exhibit 2). A large increase in capital spending, while positive for GDP numbers, would make us more worried about the potential downside for earnings. The reason is that fixed costs, like a depreciation burden on cost of goods sold (particularly for shorter asset-life industries), can cause material downside to earnings in a revenue shortfall. But this doesn't appear likely. We would wait for signs that backlogs are aging and growing or that book-to-bill ratios are meaningfully above 1.0 in the technology and industrial sectors before we'd expect to see a pickup in total capital spending. We maintain our long-held stance that capital spending will remain muted.

Parker expects the S&P 500 to hit 2,050 by the middle of 2015.

Friday, August 8, 2014

CFP Board Names Votava 2015 Chairman-Elect

Certified Financial Planner Board of Standards announced Wednesday that its Board of Directors has elected G. Joseph Votava to serve as its 2015 chairman-elect.

The Board of Directors elected Votava to the chair-elect post at its July 8-11 meeting. He will begin his duties as chairman-elect on Jan. 1, when Rich Rojeck begins his term as 2015 chairman.

“Joe has already made a significant impact on the financial planning profession through his efforts to raise awareness of the profession and advocate on behalf of it,” said current Board Chairman Ray Ferrara. “He will harness his extensive leadership experience to sustain CFP Board’s mission of benefitting the public by upholding the CFP certification as the recognized standard of excellence in personal financial planning.”

Votava added in the same statement that “between the launch of the latest phrase of the Public Awareness Campaign and the Women’s Initiative (WIN) to increase the ranks of female CFP professionals, CFP Board has taken on some exciting initiatives to foster the growth and advancement of our profession. I am honored to help lead CFP Board as we continue to work to strengthen our organization and the CFP certification.”

Votava is currently CEO of Seneca Financial Advisors LLC, which has offices in Rochester, N.Y., and Washington.

From 1985 to February 2010, Votava was a partner serving corporate executives and closely held businesses at Nixon Peabody LLP. During his tenure, Votava was the founding president of the law firm’s subsidiary, Nixon Peabody Financial Advisors LLC.

Prior to joining Nixon Peabody in 1985, he served as a certified public accountant specializing in taxation at Coopers & Lybrand, an international accounting and consulting firm. Votava formerly held chairman positions on Financial Planning Association’s National Board of Directors, and the National Endowment for Financial Education’s Board of Trustees, as well as FPA’s International Advisory Council and CFP Board’s Pubic Policy Council.

He was an honorary director of the Japan Academic Society for Financial Planning from 2000 to 2002 and also participated in an international commission to promote the growth and development of financial planning in South America, Europe, Africa and Asia.

Votava has a J.D. from University Dayton School of Law and a B.B.A. from Siena College.

---

Check out New Hire Roundup: Altegris Names Murphy Deputy CIO on ThinkAdvisor.

Monday, August 4, 2014

Lego cashes in on sexism critiques

How LEGO builds toys kids want NEW YORK (CNNMoney) Lego sure knows how to cash in on criticism.

How LEGO builds toys kids want NEW YORK (CNNMoney) Lego sure knows how to cash in on criticism. Seven year old Charlotte Benjamin penned a letter that went viral in January, criticizing the company for the lack of professional female Legos.

This month, the toy manufacturer rolled out a new set called the Research Institute created by female geophysicist, Ellen Kooijman.

The set, which costs $20, features three female scientists -- one paleontologist, one astronomer, and one chemist.

It seems to address many of Charlotte's concerns.

"All the girls did was sit at home, go to the beach, and shop, and they had no jobs but the boys went on adventures, worked, saved people, and had jobs, even swam with sharks," she wrote. " I want you to make more Lego girl people and let them go on adventures and have fun ok!?! Thank you."

The set launched on August 1 and was sold out on Lego's website by Monday. The company wouldn't say how many of the sets it's sold so far, but a spokesman said it was "produced in a limited number for select retailers." It's also for sale in Lego store and at Legoland amusement parks and discovery centers in the US and Canada.

This isn't Lego's first attempt to go after the female market -- it introduced Lego Friends in December 2011, targeted specifically to girls. Those sets feature everything from a bakery to a pet salon and a juice bar.

But there's a real shortage of women in science and technology fields. According to Girls Who Code, an organization devoted to bridging the computer science skills gender gap, women earn a mere 12 percent of computer science degrees. That's down from 1984, when the figure stood at 37 percent.

"Studies show that girls in adolescence start to lose their confidence," said Nathalie Molina Niño, co-founder of Entrepreneurs@Athena, a Barnard College initiative for women entrepreneurs. "That means...you have to catch them before then."

Friday, August 1, 2014

How Being Out of the Money Can Bring You Lots of Money When Using Binaries

Out of the Money, (OTM) binaries have a special advantage over their siblings, the At the Money (ATM) and especially the In the Money (ITM) binary. With the right priced OTM binary, you don’t need a stop loss!

That’s right, of course you always first consider if the risk of the binary is within your limits, but if the amount to put up for the binary is low enough, there is no need for a stop loss. That means putting your trade on, planning your take profit exit point (which you can exit at any time trading Nadex!), and then moving on to look for more great trades.

In this series, we have covered binaries being ATM and ITM. Here we will go over the advantages and disadvantages of binaries OTM, and the best time to trade them.

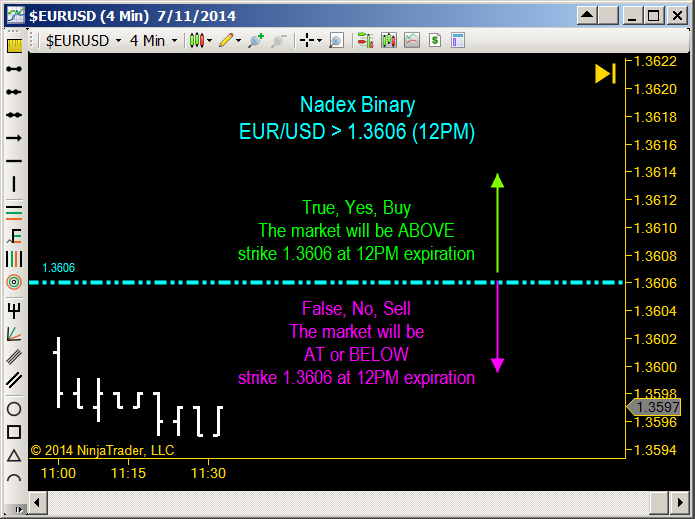

For those who don’t know, a binary is an option. When you trade it you are essentially answering the true or false statement of the binary. For example, take this Nadex binary EUR/USD >1.3606 12PM. If you were going to buy it, you would be saying this statement is true.

The underlying market EUR/USD will be ABOVE or greater than, the Nadex binary strike price 1.3606, at the expiration time 12PM. If you were going to sell it, you would be saying this statement is false. The underlying market will be AT or BELOW the strike price 1.3606 at expiration time 12PM.

Nadex binaries are worth $100. You can buy or sell them and your entry price is between $1 and $99. When you buy the binary, the entry price is your total possible risk, and the amount you put up for the trade.

The difference between $100 and your entry is your total possible profit. If you sell the binary, then it’s the inverse: the difference between $100 and your entry is your total risk, and the amount you put up for the trade.

Your entry price is your total possible profit. When the binary is settled, you receive back what you put up for the trade, plus or minus your profit or loss.

NADEX Binaries

BUY:

Binary Entry Price = Total Possible Risk = Amount Put Up for Trade

$100 – Binary Entry Price = Total Possible Profit

Settlement = Amount Put Up for Trade +/- Profit or Loss

SELL:

$100 – Binary Entry Price = Total Possible Risk = Amount Put Up for Trade

Binary Entry Price = Total Possible Profit

Settlement = Amount Put Up for Trade +/- Profit or Loss

With Nadex, the great advantage is you can exit to take profit at any time; you don’t have to wait until expiration. In fact, as we demonstrated in a previous article, to profit over time with Nadex binaries, it’s necessary to exit and take profit.

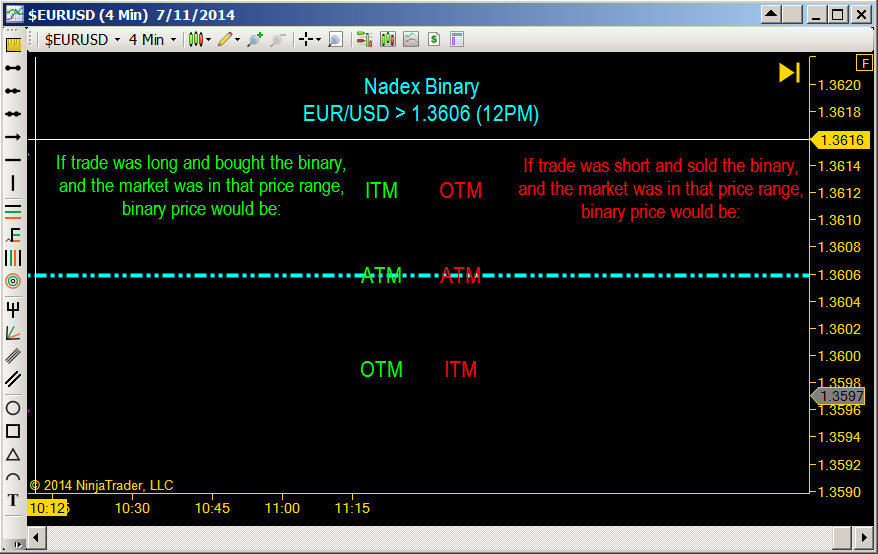

When the binary is priced at or around $50, then the underlying market is right at the strike price of the binary. Using the example above, if EUR/USD were priced at or around $50, then it would be considered ATM. At that price, it shows there is a 50/50 chance that the market could go up or down at that point, and therefore, the probability of it expiring profitable or ITM is 50%.

Now, as the underlying market moves in the direction of your trade (up if you are long or down if you are short), the amount you put up to enter the binary trade becomes more expensive or higher and the binary then is considered ITM. There is a higher probability at that point, that your trade will expire ITM. ITM would be at $100 if you are long or 0 if you are short.

You should ask yourself, “If the underlying market were on the other side of the binary’s strike price, from the direction you were to take the trade, shouldn’t the risk to trade the binary be somewhere under $45 or less?”

The probability of an OTM binary expiring profitable at expiration is low. It has so much farther to move to expire profitably, compared to an ATM or an ITM binary. That is its disadvantage. So, yes, the amount to put up or risk for the OTM binary will also be low. Hence, its name Out of the Money. An OTM option has no intrinsic value, only extrinsic or time value.

This brings us to the biggest advantages of an OTM binary: because of the low amount to put up for entry, and with low enough risk, it means you don’t need a stop loss. There is no worry then, about having to manage risk once the trade is placed. An OTM binary also has lots of possibility to pro