Coffee prices have decreased over the last few months after a large increase in 2011. This benefited coffee sellers, which had been fighting the pressures of rising coffee costs. The price drop has also benefited coffee drinkers since the coffee sellers passed the benefits on to their customers by lowering their coffee prices.

However, the news has not been all happy for J.M. Smucker (SJM), which manufactures branded-food products. Its third-quarter numbers came in below analysts' expectations, which sent its stock price down.

The Problem

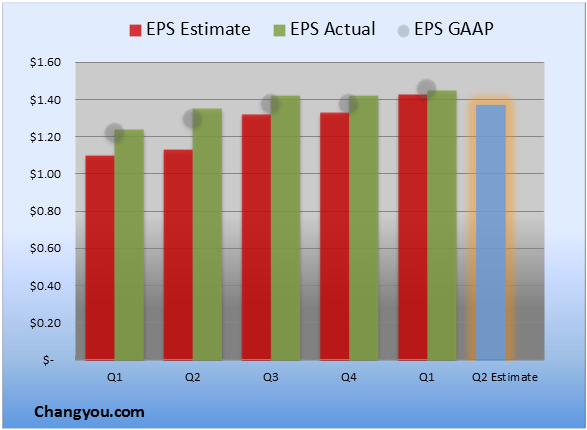

J.M. Smucker's revenue for the quarter plunged 6% from the year-ago quarter to $1.47 billion. This decline mainly came as a result of lower selling prices which affected the company's revenue from coffee (8%) as well as its U.S. foods segment (4%). Also, the company's planned exits from some parts of the international, foodservice, and natural foods segment lowered its top line.

Although volumes in the Dunkin Donuts coffee business and the Folgers brand surged 8% and 4%, respectively, volumes in other segments declined, such as peanut butter which decreased mainly because of competitive pressures from other players.

Despite the decline in revenue, J.M. Smucker's earnings increased to $1.66 per share from $1.47 per share in the year-ago period. This mainly occurred because of lower commodity costs and efficient cost-management efforts undertaken by the company. Lower input costs also led to a widening of the gross margin to 37.2% from 34.4% in the year-ago period.

Changing Preferences

Consumer tastes and preferences have changed as shoppers shift toward healthier and natural food options. As the popularity of organic and natural food increases, other vendors have also jumped into providing such items. Therefore, J.M. Smucker acquired Enray in August last year. Enray provides premium and organic grain products and Smucker's acquired it in order to strengthen its existing natural-food portfolio. Also, the company expects that the buyout will add $45 million to its revenue every year.

Similarly, peer General Mills (GIS) made a few additions to its business in order to enhance its presence in the growing healthy food market. Its acquisitions included Food Should Taste Good in February 2012, Yoplait in May 2012, and Yoki Alimentos in August 2012. It has also introduced new products such as Old El Paso and Fiber One lemon bars in order to attract more customers. Despite such efforts, General Mills has not been able to increase its top line, as its latest quarterly results could not meet investors' expectations. However, the branded-food company plans to add more products and control its costs so it affirmed its previously given outlook.

On the other hand, food manufacturer TreeHouse Foods (THS) has witnessed higher demand for its products. Its fourth-quarter revenue surged 11.4% over last year as revenue clocked in at $660.3 million. The acquisitions of Cains Foods and Associated Brands last year and an increase in volumes drove this revenue gain. The company also recently acquired Associated Brands, which added to its private-label food product portfolio. Also, TreeHouse's launch of specialty teas enabled it to expand its single-serve coffee business. Hence, this company provides tough competition to other food players.

Points for the Future

Although J.M. Smucker posted disheartening numbers and faces stiff competition from its peers, it has made certain moves which can turn things around. Along with the benefits of its acquisitions, Smucker plans to launch some new products which should attract customers.

The retailer plans to introduce blended fruit pouches in its snacks segment. The company will launch these products under the name of J.M. Smucker's Fruitful and they will enhance its fruit-spreads product category. This shows the company's efforts to cater to the health-conscious needs of consumers.

The company has also developed stronger marketing campaigns with more impact. In order to increase consumer interest, J.M. Smucker has sponsored eight Olympic champions who will be featured in all of its promotions and advertisements. Hence, this should benefit the food retailer.

However, the company did lower its outlook for the current fiscal year. It now expects its annual revenue to decrease by 5% and expects earnings in the range of $5.55 to $5.60 per share. Its guidance provided earlier called for a 2% decline in revenue and earnings between $5.72 to $5.82 per share.

Conclusion

Along with the lower-than-expected numbers, the lowered outlook added to investors' disappointment. It is difficult to say how J.M. Smucker's efforts will result in future benefits. At present, a dull quarter, increased competitive pressure, and a lowered outlook offer reasons enough to stay away from this food company.

| Currently 0.00/512345 Rating: 0.0/5 (0 votes) | |

Subscribe via Email

Subscribe RSS Comments Please leave your comment:

More GuruFocus Links

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

RSS Feed  | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

MORE GURUFOCUS LINKS

| Latest Guru Picks | Value Strategies |

| Warren Buffett Portfolio | Ben Graham Net-Net |

| Real Time Picks | Buffett-Munger Screener |

| Aggregated Portfolio | Undervalued Predictable |

| ETFs, Options | Low P/S Companies |

| Insider Trends | 10-Year Financials |

| 52-Week Lows | Interactive Charts |

| Model Portfolios | DCF Calculator |

| RSS Feed | Monthly Newsletters |

| The All-In-One Screener | Portfolio Tracking Tool |

SJM STOCK PRICE CHART

97.46 (1y: -6%) $(function(){var seriesOptions=[],yAxisOptions=[],name='SJM',display='';Highcharts.setOptions({global:{useUTC:true}});var d=new Date();$current_day=d.getDay();if($current_day==5||$current_day==0||$current_day==6){day=4;}else{day=7;} seriesOptions[0]={id:name,animation:false,color:'#4572A7',lineWidth:1,name:name.toUpperCase()+' stock price',threshold:null,data:[[1367298000000,103.23],[1367384400000,102.11],[1367470800000,102.89],[1367557200000,103.56],[1367816400000,102.55],[1367902800000,103.87],[1367989200000,103.84],[1368075600000,102.23],[1368162000000,103.63],[1368421200000,104.12],[1368507600000,104.53],[1368594000000,104.01],[1368680400000,103.32],[1368766800000,102.58],[1369026000000,101.93],[1369112400000,102.11],[1369198800000,102.51],[1369285200000,102.47],[1369371600000,103.22],[1369717200000,104.52],[1369803600000,103.02],[1369890000000,102.65],[1369976400000,100.96],[1370235600000,102.18],[1370322000000,102.64],[1370408400000,102.37],[1370494800000,98.38],[1370581200000,101.39],[1370840400000,100.24],[1370926800000,100.51],[1371013200000,100.83],[1371099600000,102.17],[1371186000000,103.01],[1371445200000,103.24],[1371531600000,103.66],[1371618000000,102.38],[1371704400000,99.98],[1371790800000,100.71],[1372050000000,99.81],[1372136400000,100.9],[1372222800000,101.64],[1372309200000,102.85],[1372395600000,103.15],[1372654800000,104.08],[1372741200000,103.15],[1372827600000,102.59],[1373000400000,103.12],[1373259600000,104.37],[1373346000000,104.62],[1373432400000,104.53],[1373518800000,105.93],[1373605200000,106.01],[1373864400000,106.66],[1373950800000,107.16],[1374037200000,106.58],[1374123600000,107.39],[1374210000000,108.16],[1374469200000,108.79],[1374555600000,109.68],[1374642000000,109.51],[1374728400000,110.72],[1374814800000,111.54],[1375074000000,112.05],[1375160400000,112.39],[1375246800000,112.52],[1375333200000,113.67],[1375419600000,113.97],[1375678800000,114.36],[1375765200000,114.23],[1375851600000,113.57],[1375938000000,113.06],[1376024400000,113.3],[1376283600000,113.51],[1376370000000,113.91],[1376456400000,112.57],[1376542800000,110.43],[1376629200000,110.32],[1376888400000,109.06],[1376974800000,109.1],[1377061200000,107.79],[1377147600000,107.49],[1377234000000,108.46],[1377493200000,107.5],[137757! 9600000,106.57],[1377666000000,105.32],[1377752400000,105.8],[1377838800000,106.14],[1378184400000,105.39],[1378270800000,106.25],[1378357200000,106.78],[1378443600000,105.99],[1378702800000,108.14],[1378789200000,108.91],[1378875600000,107.78],[1378962000000,107.27],[1379048400000,107.87],[1379307600000,107.92],[1379394000000,108.3],[1379480400000,108.48],[1379566800000,107.68],[1379653200000,107.14],[1379912400000,106.56],[1379998800000,106.39],[1380085200000,105.86],[1380171600000,105.69],[1380258000000,104.79],[1380517200000,105.04],[1380603600000,105.41],[1380690000000,104.95],[1380776400000,104.97],[1380862800000,105.93],[1381122000000,105.78],[1381208400000,105.58],[1381294800000,104.38],[1381381200000,106.51],[1381467600000,106.6],[1381726800000,106.73],[1381813200000,105.97],[1381899600000,107.5],[1381986000000,108.44],[1382072400000,107.88],[1382331600000,106.86],[1382418000000,108.73],[1382504400000,108.85],[1382590800000,109.6],[1382677200000,110.36],[1382936400000,112.2],[1383022800000,112.9],[1383109200000,111.5],[1383195600000,111.21],[1383282000000,111.01],[1383544800000,110.62],[1383631200000,110.69],[1383717600000,111.87],[1383804000000,107.61],[1383890400000,108.61],[1384149600000,107.64],[1384236000000,107.41],[1384322400000,107.93],[1384408800000,108.93],[1384495200000,109.35],[1384754400000,108.91],[1384840800000,108.59],[1384927200000,101.49],[1385013600000,103.02],[1385100000000,103.95],[1385359200000,104.31],[1385445600000,105.62],[1385532000000,105.61],[1385704800000,104.24],[1385964000000,104.45],[1386050400000,104.98],[1386136800000,104.75],[1386223200000,102.29],[1386309600000,104.32],[1386568800000,104.88],[1386655200000,103.2],[1386741600000,103.99],[1386828000000,101.38],[1386914400000,100.41],[1387173600000,101.6],[1387260000000,101.1],[1387346400000,101.86],[1387432800000,101.95],[1387519200000,102.12],[1387778400000,101.64],[1387864800000,102.36],[1388037600000,102.99],[1388124000000,103.18],[1388383200000,103.65],[1388469600000,103.62],[1388642400000,102.03],[13887288! 00000,101! .51],[1388988000000,100.9],[1389074400000,101.52],[1389160800000,98.17],[1389247200000,97.98],[1389333600000,98.42],[1389592800000,97.39],[1389679200000,99.34],[1389765600000,98.69],[1389852000000,98.55],[1389938400000,97.2],[1390284000000,97.2],[1390370400000,98.45],[1390456800000,98.08],[1390543200000,97.97],[1390802400000,98.63],[1390888800000,99.31],[1390975200000,97.11],[1391061600000,97.86],[1391148000000,96.39],[1391407200000,93.93],[1391493600000,93.71],[1391580000000,92.82],[1391666400000,93.59],[1391752800000,93.37],[1392012000000,93.7],[1392098400000,94.03],[1392184800000,93.71],[1392271200000,95.14],[1392357600000,91.81],[1392703200000,95.31],[1392789600000,95.55],[1392876000000,98.28],[1392962400000,97.94],[1393221600000,98.7],[1393308000000,99.01],[1393394400000,98.61],[1393826400000,99.05],[1393912800000,99.27],[1393999200000,98.43],[1394085600000,97.63],[1394172000000,97.54],[1394427600000,97.21],[1394514000000,96.55],[1394600400000,97.98],[1394686800000,96.99],[1394773200000,96.18],[1395032400000,96.12],[1395118800000,97.72],[1395205200000,96.14],[1395291600000,96.7],[1395378000000,96.02],[1395637200000,96.21],[1395723600000,95.94],[1395810000000,95.93],[1395896400000,96.07],[1395982800000,96.48],[1396328400000,97.14],[1396414800000,97.79],[1396501200000,97.9],[1396587600000,97.55],[1396846800000,97.9],[1396933200000,97.11],[1397019600000,97.23],[1397106000000,95.5],[1397192400000,94.33],[1397451600000,95.39],[1397538000000,95.08],[1397624400000,96.83],[1397710800000,96.7],[1398056400000,96.73],[1398142800000,96.93],[1398229200000,96.42],[1398315600000,96.99],[1398402000000,96.02],[1398661200000,97.46],[1398784745000,97.46],[1398784745000,97.46],[1398697399000,97.46]]};var reporting=$('#reporting');Highcharts.setOptions({lang:{rangeSelectorZoom:""}});var chart=new Highcharts.StockChart({chart:{renderTo:'container_chart',marginRight:20,borderRadius:0,events:{load:function(){var chart=this,axis=chart.xAxis[0],buttons=chart.rangeSelector.buttons;function reset_all_buttons(){$.each(chart.ra! ngeSelect! or.buttons,function(index,value){value.setState(0);});series=chart.get('SJM');series.remove();} buttons[0].on('click',function(e){chart.showLoading();reset_all_buttons();chart.rangeSelector.buttons[0].setState(2);var extremes=axis.getExtremes();$.getJSON('/modules/chart/price_chart_json.php?symbo

First, understand the purpose of your investment. Is it a long-term core holding that you are not going to be trading out of? Is it a market play? Are you looking to just get in and get out? Is it a temporary allocation that you might want to adjust within the next year or two?

First, understand the purpose of your investment. Is it a long-term core holding that you are not going to be trading out of? Is it a market play? Are you looking to just get in and get out? Is it a temporary allocation that you might want to adjust within the next year or two? This one is crucial as well. Are you using a lump sum to get in the market, or are you investing on a regular monthly basis?

This one is crucial as well. Are you using a lump sum to get in the market, or are you investing on a regular monthly basis?.jpg) Costs can destroy your return, so you should evaluate every possibility. When looking at your two investment options, two fees come into play: transaction! fees to ! purchase and management fees. Using the information that you determined on your purpose and how you are going to buy, come up with an estimated cost per each type of transaction.

Costs can destroy your return, so you should evaluate every possibility. When looking at your two investment options, two fees come into play: transaction! fees to ! purchase and management fees. Using the information that you determined on your purpose and how you are going to buy, come up with an estimated cost per each type of transaction.

Related PHOT A Look At 2014's Leading Cannabis Stocks (Part II) Marketfy to Host the 1st Annual Cannabis Investor Conference

Related PHOT A Look At 2014's Leading Cannabis Stocks (Part II) Marketfy to Host the 1st Annual Cannabis Investor Conference